a16z: 5 Principles of Cryptocurrency Custody 1. **Security**: Implement industry-leading security measures to protect assets from theft and unauthorized access. 2. **Compliance**: Adhere to all relevant regulations and compliance requirements to ensure

Original Article Title: Holding the future: Custody principles for a tokenized world

Original Article Authors: Scott Walker, Kate Dellolio, David Sverdlov

Translated by: Luffy, Foresight News

Registered Investment Advisors (RIAs) investing in crypto assets face a dilemma of unclear regulations and limited asset custody options. What's more complex is that crypto assets come with ownership and transfer risks different from the assets RIAs have traditionally been responsible for. RIAs' internal teams (operations, compliance, legal, etc.) are struggling to find willing and compliant third-party custodians to meet their expectations. Despite their efforts, they find it challenging to identify qualified custodians, leading RIAs to self-custody these assets. As a result, current crypto asset custody faces unique legal and operational risks.

What the crypto industry needs is a principled approach to help institutional investors safeguard crypto assets. In response to the recent Securities and Exchange Commission (SEC) request for information, we have developed some principles that, if implemented, would extend the objectives of the Investment Advisers Act custody rule to the new category of crypto assets.

How Crypto Asset Custody Differs

The control of traditional assets by their holders means that others do not have control. However, this is not the case with crypto assets, where multiple entities may have access to the private keys associated with a set of crypto assets.

Crypto assets also often come with various intrinsic economic and governance rights crucial to the assets. Traditional debt or securities can passively earn income (such as dividends or interest), and holders do not need to transfer the assets or take any further action after acquiring them. In contrast, crypto asset holders may need to take actions to unlock specific income or governance rights associated with the assets. Depending on the capabilities of the third-party custodian, RIAs may need to temporarily move these assets out of custody to unlock these rights. For example, some crypto assets can earn income through staking or yield farming, or have voting rights on protocol or network upgrade proposals. These differences from traditional assets pose new challenges to crypto asset custody.

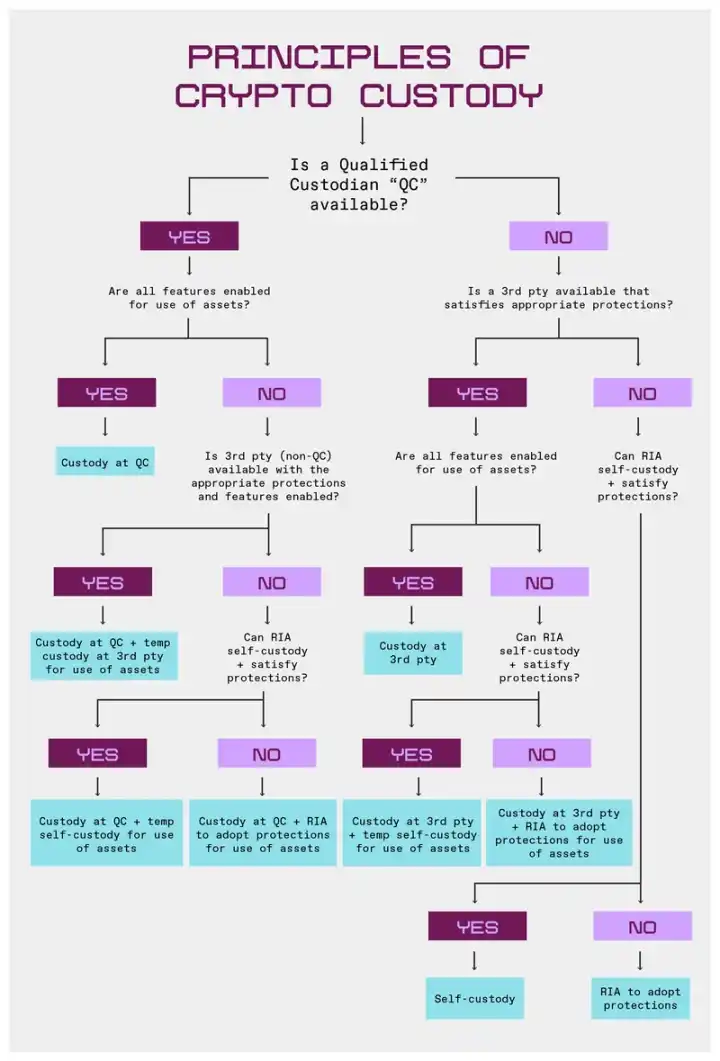

To facilitate determining when self-custody is appropriate, we have created this flowchart.

Principles

The principles we present here aim to demystify custody for RIAs while maintaining their responsibility to protect client assets. The current market for qualified custodians focusing on crypto assets (such as banks or broker-dealers) is extremely narrow. Therefore, our main focus is on whether the custodial entity has the capability to provide the substantive protective measures we believe are necessary for custody of crypto assets, rather than just the entity's legal status as a qualified custodian under the Investment Advisers Act.

We suggest that RIAs capable of meeting substantive protective measures may consider self-custody as an option when a third-party custodial solution that meets these requirements or supports economic and governance rights is unavailable.

Our goal is not to expand the scope of custody rules beyond securities. These principles apply to crypto assets that are considered securities and establish standards for RIAs' fiduciary duty for other asset types. RIAs should seek to hold non-security crypto assets under similar conditions and document custody practices for all assets, including reasons for significant differences in custody practices for different asset types.

Principle 1: Legal Status Should Not Determine Eligibility of Crypto Asset Custodians

Legal status and protective measures associated with specific legal statuses are crucial for a custodian's clients, but when it comes to crypto asset custody, this is not the only consideration. For example, federally chartered banks and broker-dealers are bound by custodial regulations that provide strict protections for clients, but state-chartered trust companies and other third-party custodians can also offer a similar level of protection.

A custodian's registration should not be the sole determining factor of its eligibility to custody crypto asset securities. In the crypto space, the scope of "qualified custodian" should be expanded to include:

- State-chartered trust companies (meaning they do not need to meet the "bank" definition standard under the Investment Advisers Act besides being subject to state or federal banking agency oversight and examination);

- Any entity registered under (proposed) federal crypto market structure legislation;

- Any other entity that can demonstrate adherence to strict client protection standards, regardless of its registration status.

Principle 2: Crypto Asset Custodians Should Establish Appropriate Protective Measures

Regardless of the technical tools used, custodians should implement specific protective measures around crypto asset custody. These measures include:

1. Segregation of Authority: Crypto asset custodians should not be able to withdraw crypto assets without the cooperation of RIAs.

2. Asset Segregation: Crypto asset custodians should not commingle assets held for RIAs with assets held for other entities. However, registered broker-dealers may use a single omnibus wallet, provided that they always maintain up-to-date records of ownership of these assets and promptly disclose the situation to the relevant RIAs.

3. Hardware Custody: The cryptographic asset custodian shall not use any custody hardware or other tools that pose a security risk or have a compromised risk.

4. Audit: The cryptographic asset custodian shall undergo at least annual financial and technical audits. Such audits shall include:

Financial audit by a PCAOB registered auditor:

Service Organization Control (SOC) 1 audit; SOC 2 audit; as well as confirmation, measurement, and reporting of cryptographic assets from a holder's perspective;

Technical audit:

ISO 27001 certification; penetration testing; as well as testing of disaster recovery procedures and business continuity planning.

5. Insurance: The cryptographic asset custodian shall have sufficient insurance coverage, or if insurance cannot be obtained, shall establish sufficient reserves.

6. Disclosure: The cryptographic asset custodian must annually provide RIAs with a major risk list related to its custody of cryptographic assets, as well as related written supervisory procedures and internal control measures to mitigate these risks. The cryptographic asset custodian shall review this quarterly to determine if disclosure updates are necessary.

7. Custody Jurisdiction: The cryptographic asset custodian shall not custody cryptographic assets in any jurisdiction where local laws stipulate that custodied assets will become part of the bankruptcy estate in the event of the custodian's bankruptcy.

Additionally, we recommend that the cryptographic asset custodian implement protective measures related to the following processes at each stage:

Preparation Stage: Review and assess the cryptographic assets to be custodied, including the key generation process and transaction signing process, whether it is supported by open-source wallets or software, and the source of every piece of hardware and software used in the key management process.

Key Generation: Encryption technology should be used at various levels of this process, and multiple cryptographic keys are required to generate a private key. The key generation process should be both "horizontal" (i.e., multiple cryptographic key holders at the same level) and "vertical" (i.e., multiple levels of encryption). Finally, statutory quorum requirements should also ensure the physical presence of authenticators.

Key Storage: Keys should never be stored in plain text but only in encrypted form. Keys must be physically isolated by geographical location or different access personnel. If hardware security modules are used to store key copies, they must meet Federal Information Processing Standards (FIPS) security ratings. Strict physical isolation and authorization measures should be implemented. The cryptographic asset custodian should maintain at least two levels of encrypted redundancy to ensure operation in the event of a natural disaster, power outage, or property destruction.

Key Usage: Wallets should require authentication; in other words, they should verify the user's identity and only allow authorized parties to access the wallet. Wallets should use mature open-source cryptographic libraries. Another best practice is to avoid using one key for multiple purposes. For example, keys for encryption and signing should be kept separate. Follow the principle of "least privilege," meaning that in the event of a security breach, access to any asset, information, or operation should be limited to only the parties absolutely necessary for the system to function.

Principle 3: The Cryptocurrency Asset Custody Rule should allow registered investment advisors to exercise economic or governance rights related to custody of cryptocurrency assets

Unless otherwise directed by the client, RIAs should be able to exercise economic or governance rights related to the custody of cryptocurrency assets. During the previous SEC administration, given the uncertainty surrounding token classification, many RIAs adopted a conservative strategy of custodian all cryptocurrency assets with a qualified custodian. As mentioned earlier, the available custodian market is limited, often resulting in only one qualified custodian willing to support a particular asset.

In these cases, RIAs may seek to exercise economic or governance rights, but the cryptocurrency asset custodian may choose not to offer these rights for various reasons. In turn, RIAs feel they do not have the power to choose another third-party custodian or self-custody to exercise these rights. These economic and governance rights include staking, yield farming, or voting.

Under this principle, we advocate that RIAs should select third-party cryptocurrency asset custodians that comply with relevant protective measures so that RIAs can exercise economic or governance rights related to the custody of cryptocurrency assets. If a third party cannot meet both of these requirements simultaneously, RIAs should not be seen as breaching custody by temporarily transferring assets for self-custody to exercise these rights.

All third-party custodians should make every effort to provide RIAs with the ability to exercise these rights while the assets are still under their custody and, when authorized by RIAs, take commercially reasonable action to exercise any rights related to on-chain assets.

Prior to transferring assets out for custody in order to exercise rights related to a specific cryptocurrency asset, RIAs or custodians must first determine in writing whether those rights can be exercised without transferring the assets out of custody.

Principle 4: The Cryptocurrency Asset Custody Rule should be flexible to achieve best execution

RIAs have a best execution obligation when trading assets. To this end, RIAs may transfer assets to a cryptocurrency trading platform to ensure the best execution of that asset, regardless of the asset's or custodian's status, provided that RIAs have taken the necessary steps to ensure the security of the trading venue, or RIAs have already transferred the cryptocurrency assets to an entity regulated under the cryptocurrency market structure legislation once finalized.

As long as RIAs determine that transferring cryptographic assets to an exchange for best execution is prudent, this transfer should not be viewed as relinquishing custody. This requires RIAs to reasonably determine that the exchange is suitable for best execution. If the trade cannot be properly executed on the exchange, the assets should be immediately returned to the cryptographic asset custodian.

Principle 5: In certain circumstances, RIAs should be allowed to self-custody.

While third-party custody should still be the primary choice for cryptographic assets, in the following circumstances, RIAs should be allowed to self-custody cryptographic assets:

· RIAs determine that they cannot find a third-party custodian that meets their required security measures;

· RIAs' self-custody arrangement is at least as effective as the protections available from third-party custodians;

· Self-custody is necessary for exercising any economic or governance rights related to cryptographic assets.

When RIAs decide to self-custody cryptographic assets for these reasons, RIAs must annually confirm that the circumstances warranting self-custody have not changed, disclose the self-custody arrangement to clients, and subject such cryptographic assets to the audit requirements of the Custody Rule.

Based on these principles, the cryptographic asset custody approach ensures that RIAs can fulfill their fiduciary responsibilities while accommodating the unique characteristics of cryptographic assets. By focusing on substantive protection rather than rigid categorization, these principles provide a practical path forward to safeguarding client assets and unlocking asset functionality. As the regulatory environment evolves, clear standards based on these protective measures will enable RIAs to responsibly manage cryptographic assets.

You may also like

Latest research from 13 top universities including Cornell University: The current state, challenges, and misconceptions of the fusion of Crypto and AI

Deconstructing Anthropic: The Best AI Company, Possibly Also a Type of Organizational Invention

Apollo and Blackstone Reportedly Back $35 Billion Anthropic Chip Financing as Deal Details Remain Unclear

On June 9, according to currently available news alerts, Apollo and Blackstone Group participated in a $35 billion financing for an Anthropic “chip project.” Based on the original wording of the report, the funding has already been raised, but public information remains limited. The financing structure, use of proceeds, project entity, and whether Apollo and Blackstone participated through equity, debt, or project financing have not yet been disclosed.

Humanity Protocol Security Incident Escalates: More Than $31 Million Stolen From Related Addresses as Attacker Continues Selling H for ETH

On June 9, according to monitoring by Onchain Lens, more than $31 million has been stolen from addresses linked to Humanity Protocol, and the attack is still ongoing, with the hacker continuously swapping H tokens for ETH. Project founder Terence Kwok later confirmed the security incident on X, saying the issue involved a private key leak.

Bloomberg: As Bitcoin Weakens, Stablecoins and RWA Continue to Drive Expansion in Crypto Businesses

In June, Bloomberg reported that despite Bitcoin falling below $60,000 last week, wiping out about $235 billion in market value within seven days, and dropping close to 50% from last year’s peak, some core businesses in the crypto industry are still expanding, mainly in stablecoins, real-world asset tokenization (RWA), payments, and infrastructure. The report also noted that overall altcoin activity has contracted significantly: altcoin market capitalization has fallen from a peak of about $431 billion in November 2021 to around $170 billion, and among the tens of millions of tokens issued in recent years, fewer than 1,700 still maintain meaningful trading activity.

Galaxy Deep Research Report: How Hyperliquid's HIP-4 Upgrade Changes the Landscape of Prediction Markets?

Binance Research: RWA Market Expected to Expand Nearly 6x from Early 2025, with Public Equities and Onchain Payments Heating Up Together

In June, Binance Research said in its monthly market report that the real-world asset (RWA) market is expected to grow by about 589% from the beginning of 2025. Bond- and money market fund-related RWA expanded by about $6.5 billion, up 83% year over year, while publicly traded equity RWAs grew by about 422%. The report also noted that monthly crypto debit card transaction volume exceeded $747 million in May, up 48.6% year to date.

Japan to Assess a Framework for Yen Stablecoins and Crypto ETFs as Asia’s Compliant Payments Narrative Heats Up

Recently, according to the original report, Japan is considering the launch of yen stablecoins and cryptocurrency ETFs. Public information remains limited at this stage, and there is still no complete policy text, regulatory draft, or clear implementation timeline, so this is better characterized as a “policy discussion” rather than formal implementation. The original wording also noted that advancing stablecoin regulation in Asia is driving XRP usage and supporting growth in the XRPL ecosystem. However, based on currently available public information, there is not enough evidence to directly establish a clear causal relationship between this round of discussion in Japan and XRP or XRPL.

ZachXBT: Humanity private key leak and abnormal surge in H token should be viewed separately

On June 9, according to related disclosures, on-chain investigator ZachXBT posted an update on Humanity’s roughly $31 million security incident, saying that after further analyzing fund flows, he currently tends to believe the project team was not involved in an “inside job” or a self-staged attack. According to him, the official explanation about the private key leak was broadly accurate, but before the token unlock, the price of H had been artificially pushed higher, and the hacker later took advantage of that market environment; therefore, the private key leak and the earlier abnormal price pumping should be regarded as two separate and independent events. This reframing has shifted the market’s understanding of the nature of the incident. Earlier discussion around Humanity had focused on whether the team directly participated in the attack or used the security incident to cover up internal operations. ZachXBT’s latest remarks shift the focus from “whether it was self-theft” to “whether there were pre-unlock market structure issues.” He also questioned whether the team may have.

Morning Report | OpenAI has submitted an S-1 registration statement draft to the U.S. SEC; Morpho completes $175 million financing

Morning Report | BitMine increased its holdings by 126,971 ETH last week; trader Eugene announced his exit from the crypto market

Wang Chuan: How can one not feel anxious after the neighbor Old Wang made thirty times profit by investing in storage stocks? (Seven) - A quarter-century cycle

Cryptocurrency CEXs are flocking to sell US stocks, and traditional brokerages are facing an "uninvited guest."

$75 billion in foreign capital has fled, and South Korean retail investors have absorbed it all using leverage

Japan’s Three Megabanks Plan Joint Stablecoin Issuance in Fiscal 2026

MUFG, SMBC, and Mizuho reportedly plan to jointly issue fiat-pegged stablecoins in fiscal 2026, signaling Japan’s growing push into bank-led digital payment infrastructure.

Humanity Discloses H Token Dual-Chain Attack Details, With Losses on Ethereum and BSC Exceeding $36 Million

Humanity said the H token attack across Ethereum and BSC caused more than $36 million in losses after leaked ProxyAdmin keys enabled malicious contract upgrades and token minting.

White House Discusses CLARITY Act With Law Enforcement Ahead of Senate Vote

The White House discussed the CLARITY Act with law enforcement ahead of a Senate vote, focusing on illicit finance risks and developer protections.

Bitcoin Trading Guide 2026: Strategies for Experienced Traders

Latest research from 13 top universities including Cornell University: The current state, challenges, and misconceptions of the fusion of Crypto and AI

Deconstructing Anthropic: The Best AI Company, Possibly Also a Type of Organizational Invention

Apollo and Blackstone Reportedly Back $35 Billion Anthropic Chip Financing as Deal Details Remain Unclear

On June 9, according to currently available news alerts, Apollo and Blackstone Group participated in a $35 billion financing for an Anthropic “chip project.” Based on the original wording of the report, the funding has already been raised, but public information remains limited. The financing structure, use of proceeds, project entity, and whether Apollo and Blackstone participated through equity, debt, or project financing have not yet been disclosed.

Humanity Protocol Security Incident Escalates: More Than $31 Million Stolen From Related Addresses as Attacker Continues Selling H for ETH

On June 9, according to monitoring by Onchain Lens, more than $31 million has been stolen from addresses linked to Humanity Protocol, and the attack is still ongoing, with the hacker continuously swapping H tokens for ETH. Project founder Terence Kwok later confirmed the security incident on X, saying the issue involved a private key leak.

Bloomberg: As Bitcoin Weakens, Stablecoins and RWA Continue to Drive Expansion in Crypto Businesses

In June, Bloomberg reported that despite Bitcoin falling below $60,000 last week, wiping out about $235 billion in market value within seven days, and dropping close to 50% from last year’s peak, some core businesses in the crypto industry are still expanding, mainly in stablecoins, real-world asset tokenization (RWA), payments, and infrastructure. The report also noted that overall altcoin activity has contracted significantly: altcoin market capitalization has fallen from a peak of about $431 billion in November 2021 to around $170 billion, and among the tens of millions of tokens issued in recent years, fewer than 1,700 still maintain meaningful trading activity.